Zero-Based Budget Template for Families (Free Printable)

Every month, money comes in. Every month, money goes out. And somehow, you reach the end of the month wondering where it all went.

You’re not overspending on luxuries. You’re not living beyond your means. But you also can’t seem to get ahead. Savings accounts stay empty. Small emergencies become financial crises. And the stress of not knowing exactly where your money goes keeps you up at night.

The problem isn’t that you’re bad with money. The problem is you don’t have a system that tells every single dollar where to go.

That’s where zero-based budgeting changes everything.

A zero-based budget isn’t complicated financial jargon. It’s a simple concept: your income minus your expenses equals zero. Every dollar you earn gets assigned a job—whether that’s paying bills, building savings, or funding your kids’ activities. Nothing is left unassigned. Nothing slips through the cracks.

In this post, I’m walking you through exactly what a zero-based budget is, why it works so well for families, and how to create one using our free family budget template. You’ll learn the step-by-step process, see real examples, and get strategies for making this budget actually stick.

By the end of this post, you’ll have a complete budgeting system that finally gives you control over your money.

Let’s build your family’s financial foundation.

What Is a Zero-Based Budget?

Before we dive into the how, let’s make sure you understand the what and the why.

The Core Concept

A zero-based budget means you assign every dollar of income a specific purpose until you reach zero.

Here’s the formula:

Income – Expenses – Savings – Debt Payments = $0

This doesn’t mean you spend all your money. It means you intentionally direct all your money somewhere—including into savings and investments.

How It’s Different From Traditional Budgeting

Traditional budgeting:

- Track spending categories loosely

- Hope you have money left over at month’s end

- React to spending rather than direct it

- Often leaves unassigned money that gets wasted

Zero-based budgeting:

- Assign every dollar before the month begins

- Know exactly where every penny goes

- Proactively decide spending before it happens

- Ensures nothing is wasted or forgotten

Why This Works for Families

Families have complex, variable expenses. Kids’ activities, school costs, groceries, medical appointments, clothing—these change month to month. Traditional budgeting struggles with variability.

Zero-based budgeting handles variability perfectly because you rebuild your budget every month based on that month’s specific needs and income.

Example:

- January: Extra expenses for school registration fees

- February: Lower expenses, more to savings

- March: Spring break activities planned

- December: Holiday spending budgeted in advance

Each month’s budget is customized. You’re always intentional, never surprised.

The Mindset Shift

The biggest change isn’t the method—it’s how you think about money.

Old mindset: “I hope we have enough money this month”

New mindset: “I’ve told every dollar what to do this month”

Old mindset: “Where did our money go?”

New mindset: “Our money went exactly where we directed it”

Old mindset: “Budgeting is restrictive”

New mindset: “Budgeting is permission to spend on what matters”

This shift from reactive to proactive changes everything.

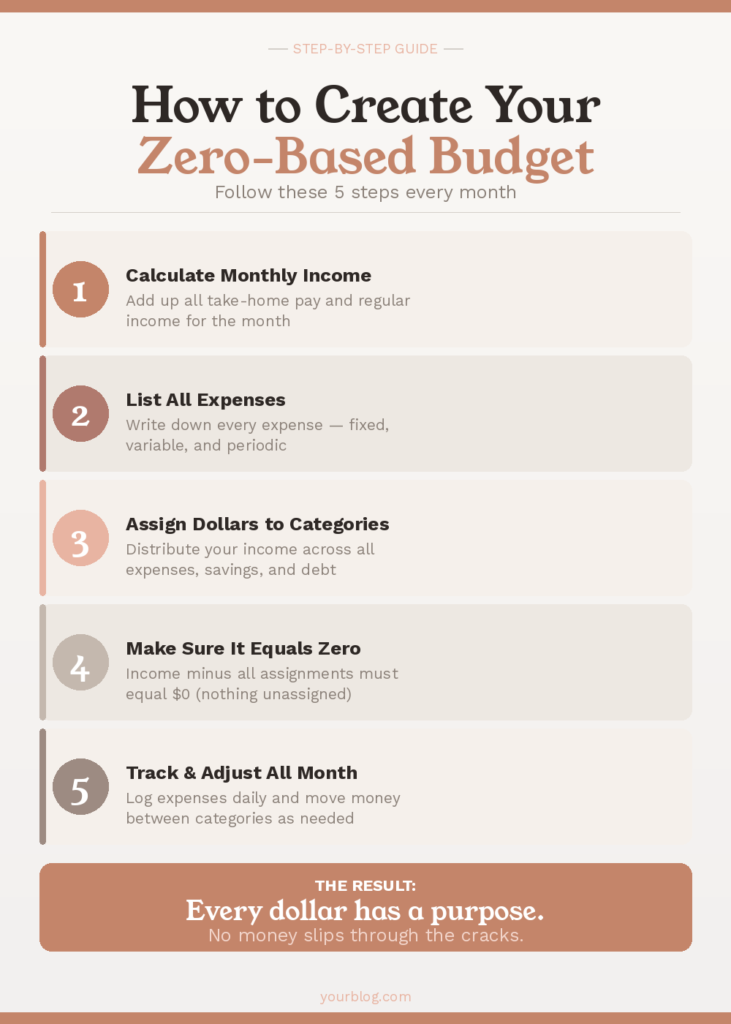

How Zero-Based Budgeting Actually Works

Let’s break down the process step by step. Don’t worry—it’s simpler than it sounds.

Step 1: Calculate Your Monthly Income

Start with your take-home pay (after taxes and automatic deductions).

If you have consistent income:

- Add up all regular paychecks for the month

- Include any side income, child support, or other regular money

If you have variable income:

- Use your lowest monthly income from the past 3 months

- Budget based on this conservative number

- Extra money in higher-income months goes to savings/debt

Example:

- Mom’s bi-weekly paycheck: $1,600 × 2 = $3,200

- Dad’s bi-weekly paycheck: $1,800 × 2 = $3,600

- Total monthly income: $6,800

Step 2: List All Your Expenses

Write down every expense you have in a month. Everything.

Fixed expenses (same every month):

- Rent/mortgage

- Car payment

- Insurance (car, home, health)

- Phone bill

- Internet

- Streaming services

- Childcare

- Loan payments

Variable expenses (change monthly):

- Groceries

- Gas

- Utilities (electric, water, gas)

- Household items

- Clothing

- Kids’ activities

- Entertainment

- Eating out

Periodic expenses (not every month):

- Car registration

- Yearly subscriptions

- Holiday spending

- Birthday gifts

- School expenses

Pro tip: Look at your last 2-3 months of bank statements to catch expenses you might forget.

Step 3: Assign Dollars to Categories

Now the magic happens. Take your income and distribute it across all your expenses.

Start with the essentials:

- Housing (rent/mortgage, utilities)

- Food (groceries, reasonable eating out)

- Transportation (car payment, gas, insurance)

- Basic necessities (phone, internet, medications)

Then add:

- Debt payments (minimums first, extra if possible)

- Savings (emergency fund, goals)

- Kids’ needs (activities, school costs, clothing)

- Personal spending (haircuts, entertainment, hobbies)

Keep assigning until you hit zero.

Step 4: The Math Must Equal Zero

Here’s what it looks like:

Income: $6,800

Expenses:

- Mortgage: $1,400

- Utilities: $200

- Groceries: $800

- Gas: $300

- Car payment: $350

- Car insurance: $180

- Phone: $120

- Internet: $80

- Childcare: $600

- Student loan: $200

- Kids’ activities: $150

- Household items: $100

- Clothing: $80

- Entertainment: $100

- Personal spending: $200

Total expenses: $4,860

Remaining: $6,800 – $4,860 = $1,940

Now assign that $1,940:

- Emergency fund: $500

- Christmas sinking fund: $200

- Vacation savings: $300

- Extra debt payment: $500

- Car repair fund: $200

- Kids’ college fund: $240

Total assigned: $1,940

Final calculation: $6,800 – $4,860 – $1,940 = $0

Every dollar has a job. Nothing is left floating.

Step 5: Track and Adjust Throughout the Month

A zero-based budget isn’t set-and-forget. You’ll need to adjust as the month progresses.

When unexpected expenses come up:

- Decide where that money comes from

- Reduce another category to cover it

- Update your budget to reflect the change

Example: Car needs a $200 repair mid-month.

Don’t panic—adjust:

- Reduce entertainment budget from $100 to $50

- Reduce eating out from $150 to $100

- Pull $50 from miscellaneous

The $200 is now covered. Your budget still equals zero. You’ve just redistributed money.

Creating Your Family Budget Template

Now let’s build your actual budget. You can use our free printable template or create your own.

Essential Categories for Families

Your family budget template should include these core categories:

Housing:

- Rent or mortgage

- Property tax (if not in mortgage)

- HOA fees

- Home insurance

- Utilities (electric, gas, water, trash)

- Home maintenance fund

Transportation:

- Car payment(s)

- Gas

- Car insurance

- Registration/tags

- Maintenance and repairs

- Public transportation

Food:

- Groceries

- School lunches

- Eating out/takeout

- Coffee shops

Family & Kids:

- Childcare/daycare

- School tuition or fees

- Kids’ activities (sports, music, etc.)

- School supplies

- Kids’ clothing

- Allowance

- Diapers/baby supplies (if applicable)

Personal:

- Adult clothing

- Haircuts/salon

- Personal care items

- Gym membership

- Hobbies

- Phone bill

- Subscriptions (streaming, apps, magazines)

Health:

- Health insurance premiums

- Medications

- Co-pays and medical expenses

- Vision/dental expenses

Debt:

- Credit card payments

- Student loans

- Personal loans

- Medical debt

Savings:

- Emergency fund

- Retirement contributions

- Kids’ college fund

- Specific goal savings (vacation, home, car)

Sinking Funds:

- Christmas/holidays

- Birthdays

- Car repairs

- Home repairs

- Annual subscriptions

- Vet bills

Giving:

- Charitable donations

- Gifts

- Religious contributions

Monthly vs. Annual Expenses

The trap: Forgetting about annual or irregular expenses, then getting blindsided.

The solution: Sinking funds.

How it works:

- Calculate the annual expense

- Divide by 12

- Budget that amount every month

- When the expense comes, you’re ready

Example:

- Car registration: $180/year ÷ 12 = $15/month

- Christmas shopping: $600/year ÷ 12 = $50/month

- Amazon Prime: $139/year ÷ 12 = $11.58/month

- Kids’ summer camp: $480/year ÷ 12 = $40/month

Budget these monthly amounts into your zero-based budget. When the expenses hit, the money is already there.

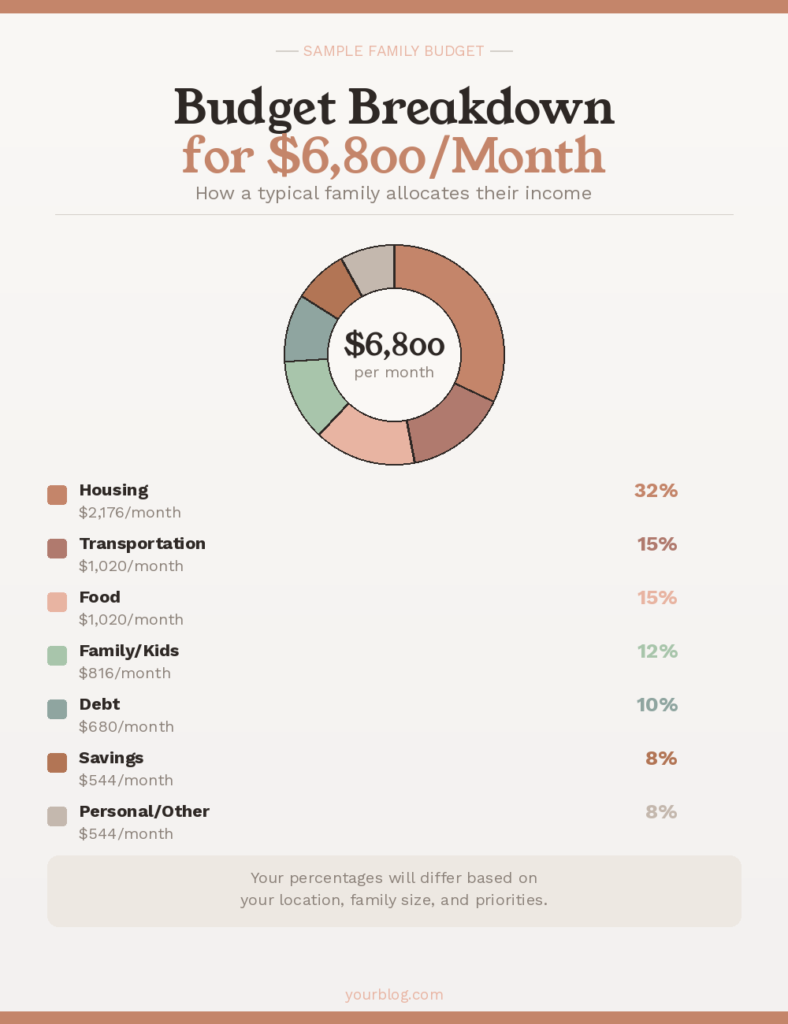

Sample Family Budget Breakdown

Here’s what a realistic family budget might look like for a household earning $6,800/month:

Housing (32%): $2,176

- Mortgage: $1,400

- Utilities: $200

- Home insurance: $100

- HOA: $76

- Maintenance fund: $400

Transportation (15%): $1,020

- Car payment: $350

- Gas: $300

- Insurance: $180

- Maintenance: $100

- Registration fund: $15

- Future car fund: $75

Food (15%): $1,020

- Groceries: $800

- Eating out: $150

- School lunches: $70

Family/Kids (12%): $816

- Childcare: $600

- Activities: $150

- Clothing: $66

Debt (10%): $680

- Student loan: $200

- Credit card: $480 (aggressive payoff)

Savings (8%): $544

- Emergency fund: $300

- Retirement: $144

- College fund: $100

Personal/Other (8%): $544

- Phone: $120

- Internet: $80

- Subscriptions: $50

- Personal spending: $194

- Entertainment: $100

TOTAL: $6,800 (100%)

Your percentages will differ based on your location, family size, and priorities. This is just an example.

Common Zero-Based Budgeting Challenges (And Solutions)

Let’s address the obstacles you’ll face—because you will face them.

Challenge #1: “This takes too much time”

Reality check: The first budget takes 60-90 minutes. Every budget after that takes 20-30 minutes.

Solution:

- Use our template to speed up the process

- Set up categories once, reuse them every month

- Block calendar time on the last Sunday of each month to plan next month

- Remember: 30 minutes of planning saves hours of stress

Challenge #2: “My income varies every month”

This is actually perfect for zero-based budgeting.

Solution:

- Budget based on your minimum expected income

- When you earn more, immediately assign the extra money (savings, extra debt payment, specific goal)

- Build a larger emergency fund to smooth out low-income months

- Consider keeping one month’s expenses in checking as a buffer

Challenge #3: “My partner won’t stick to it”

Budgeting only works if both partners commit.

Solution:

- Create the budget together, not solo

- Both partners need input on spending categories

- Schedule a weekly 10-minute money check-in

- Use a budgeting app where both can see real-time spending

- Agree on personal “fun money” amounts—no questions asked about how it’s spent

Challenge #4: “Unexpected expenses ruin everything”

Unexpected expenses are actually predictable—you just don’t know when.

Solution:

- Build a $1,000 starter emergency fund ASAP

- Create sinking funds for predictable “unpredictables” (car repairs, medical, home)

- When true emergencies happen, use the emergency fund, then rebuild it

- Adjust other categories to accommodate—the budget is flexible

Challenge #5: “I overspend in certain categories”

This is the most common issue.

Solution:

- Track spending daily (app or envelope system)

- Use cash for problem categories (groceries, eating out)

- When you hit the limit, you’re done spending—find creative solutions

- Ask yourself: “Is this purchase worth reducing another category?”

- Over time, you’ll naturally adjust to the limits

Making Your Zero-Based Budget Actually Work

Knowledge is worthless without implementation. Here’s how to make this stick.

Week 1: Set Up Your System

Choose your method:

- Printable template (free download below—fill in by hand)

- Spreadsheet (Google Sheets or Excel)

- Budgeting app (YNAB, Monarch Money, Goodbudget)

- Combination (digital tracking, printed visual reminder)

Do your first budget:

- Gather last month’s bank statements

- List all income and expenses

- Create your categories

- Assign every dollar

- Make sure income – expenses = $0

Set up tracking:

- Download a spending tracker app

- Create a receipt system

- Designate who tracks what in your household

Week 2-4: Track and Adjust

Daily habit: Log every expense (takes 2-3 minutes)

Weekly habit: Review spending vs. budget (takes 10 minutes)

- Are you staying in your categories?

- Do you need to move money between categories?

- What’s working? What’s not?

Monthly habit: Evaluate and rebuild for next month

- What surprised you this month?

- What categories need adjustment?

- Are you making progress on goals?

Month 2-3: Refine Your Categories

Your first budget will be wrong. That’s normal.

Adjust based on reality:

- You budgeted $600 for groceries but consistently spend $750? Increase it.

- You budgeted $200 for gas but only need $120? Lower it and redirect the difference.

- You forgot about pet expenses? Add that category.

Your budget should reflect your actual life, not an idealized version.

Month 4+: Experience the Benefits

By month 4, you’ll notice:

- You stop running out of money mid-month

- “Unexpected” expenses don’t panic you

- You know exactly how much you can spend on anything

- Savings are actually growing

- Debt is decreasing

- Money fights with your partner decrease

- Financial stress significantly reduces

This is when the system becomes automatic and you wonder how you ever functioned without it.

Zero-Based Budgeting for Different Income Levels

This system works whether you’re living paycheck to paycheck or have comfortable income.

Tight Budget (Just Covering Basics)

If every dollar is spoken for:

- Focus heavily on the Four Walls: food, shelter, utilities, transportation

- Minimize everything else temporarily

- Even $25/month to savings counts

- Use sinking funds to prevent emergencies from destroying your budget

- Every raise or extra income goes straight to emergency fund until you have $1,000

The goal: Stop the paycheck-to-paycheck cycle by building a buffer.

Moderate Budget (Covering Needs + Some Wants)

If you have some flexibility:

- Essentials covered easily

- Some money for wants and fun

- Building savings consistently

- Paying extra on debt

- Budget includes quality-of-life spending (activities, entertainment, hobbies)

The goal: Accelerate financial progress while enjoying life.

Comfortable Budget (Needs Met + Significant Savings)

If you have discretionary income:

- All needs met without stress

- Regular savings and investing

- Funding kids’ futures

- Enjoying hobbies and travel

- Focus on optimizing, not surviving

The goal: Intentional wealth building and generous living.

Zero-based budgeting works at every level because it’s about intentionality, not income amount.

Teaching Your Kids About Zero-Based Budgeting

Use your family budget as a teaching opportunity.

Age-Appropriate Involvement

Ages 5-7:

- Explain that money has jobs

- Let them see you checking categories

- Give them a small amount to budget (allowance split into save/spend/give)

Ages 8-12:

- Include them in family budget meetings

- Let them help categorize receipts

- Give them clothing budget—they make purchasing decisions

- Teach them about sinking funds for big wants

Ages 13-18:

- Show them the actual family budget (age-appropriate transparency)

- Give them larger category responsibility (their activities, clothing, phone)

- Help them create their own zero-based budget for job income

- Discuss trade-offs: “If we spend here, we can’t spend there”

The life skill you’re teaching is more valuable than any specific dollar amount.

Your Free Family Budget Template

We’ve created a comprehensive, printable zero-based budget template specifically for families.

What’s included:

✓ Monthly budget worksheet with all standard family categories

✓ Income tracker for multiple income sources

✓ Expense categories pre-organized and customizable

✓ Sinking fund planner for irregular expenses

✓ Debt payoff tracker to visualize progress

✓ Savings goals section for emergency fund and specific goals

✓ Weekly spending tracker to stay on target

✓ Monthly review checklist to evaluate and adjust

How to use it:

- Download and print (or save digitally if you prefer)

- Fill in your monthly income at the top

- List all expenses in the provided categories

- Assign dollar amounts until income minus expenses equals zero

- Track spending throughout the month

- Review and adjust at month’s end

- Create next month’s budget based on what you learned

Customization tips:

- Add categories specific to your family

- Remove categories you don’t need

- Adjust category order based on priority

- Make notes in margins about what’s working

Take Control of Your Family’s Finances Today

You now understand everything you need to know about zero-based budgeting:

✓ What it is and why it works

✓ Step-by-step how to create your budget

✓ Essential categories for families

✓ How to handle challenges and obstacles

✓ How to make the system stick long-term

The only thing left is to actually do it.

Not next month. Not when things are “less busy.” Not when you “have more money.”

This week.

Here’s your action plan:

Today:

- Download the free family budget template below

- Gather your income information

- Look at last month’s spending

This weekend:

- Create your first zero-based budget for next month

- Discuss with your partner

- Set up your tracking system

Next month:

- Live on your budget

- Track every expense

- Adjust as needed

Month 2:

- Refine categories based on reality

- Start building momentum

This isn’t about being perfect. Your first budget will have mistakes. Your second budget will be better. Your third will be even better.

The point is to start.

Right now, your money controls you. After implementing a zero-based budget, you’ll control your money. That shift—from reactive to proactive, from stressed to confident—changes everything.

Your family’s financial future starts with one decision: the decision to tell every dollar where to go instead of wondering where it went.

Make that decision today.

Download Your Free Zero-Based Budget Template

Ready to take control of your family’s finances?

Get instant access to our comprehensive family budget template—completely free.

This isn’t some basic spreadsheet. This is a complete budgeting system designed specifically for busy families who need a simple, sustainable way to manage money.

What you’ll receive:

- Printable zero-based budget worksheet

- Digital version for Excel/Google Sheets

- Step-by-step instruction guide

- Sample completed budget for reference

- Bonus: Monthly budget review checklist

Download now and start your first budget this weekend.

Click the link below to get your free family budget template:

[DOWNLOAD FREE ZERO-BASED BUDGET TEMPLATE]

No email required. No credit card. No strings attached. Just a free tool to help your family win with money.

Your journey to financial confidence starts now. Download the template and create your first zero-based budget today.

You’ve got this.

Ready to transform your family’s finances? Download the free zero-based budget template and start telling your money where to go instead of wondering where it went.