The $1,000 Emergency Fund Challenge: Week-by-Week Action Plan

The check engine light came on.

My stomach dropped. We had exactly $147 in our checking account, and payday was five days away. The repair estimate? $850.

I had no emergency fund. No savings. No backup plan. So I did what millions of Americans do when emergencies hit: I put it on a credit card I couldn’t afford to pay off, added $850 to our debt, and spent the next six months paying interest on a car repair.

That moment changed everything for me.

I realized that without an emergency fund, I wasn’t just broke—I was trapped. Every unexpected expense became a crisis. Every small emergency became debt. I was one car repair, one medical bill, one broken appliance away from financial disaster.

So I committed to saving $1,000 as fast as humanly possible. Not someday. Not when things were “less tight.” Immediately.

It took me 12 weeks. Twelve weeks of intense focus, creative money-finding, and saying no to things I wanted. But when I hit that $1,000 mark, everything changed. The next time an emergency hit, I had options. I had breathing room. I had security.

That $1,000 emergency fund transformed my relationship with money.

In this post, I’m giving you the exact week-by-week action plan I used to save $1000 fast—along with strategies from dozens of other moms who’ve completed this challenge successfully. This isn’t theory. These are proven tactics that work for real families with tight budgets and limited time.

If you’re living paycheck to paycheck, terrified of the next unexpected expense, this challenge is for you.

Let’s build your emergency fund—starting today.

Why $1,000 Is Your First Financial Goal

Before we dive into the weekly plan, let’s talk about why this specific number matters.

The Reality of Emergency Expenses

Most emergencies cost between $300 and $1,200:

- Car repairs: $300-1,200

- Medical co-pays and urgent care: $100-500

- Broken appliances (washer, fridge, HVAC): $200-1,000

- Unexpected vet bills: $200-800

- Urgent home repairs (plumbing, electrical): $200-1,500

- Job loss (immediate needs while finding work): $500-2,000

With $1,000 saved, you can handle the majority of common emergencies without going into debt.

Why Not More? Why Not Less?

$500 is too small – Many emergencies exceed this amount, leaving you partially covered but still needing credit

$3,000-6,000 is the ultimate goal – But if you’re living paycheck to paycheck, this feels impossible and discouraging

$1,000 is the sweet spot:

- Achievable in 8-16 weeks for most families

- Covers most emergencies completely

- Builds momentum and confidence

- Creates a foundation for bigger savings goals

Think of $1,000 as your starter emergency fund—not your final destination, but your first major financial milestone.

The Psychological Shift

Having $1,000 in the bank changes how you feel about money.

Before:

- Constant anxiety about “what if”

- Every unexpected expense is a catastrophe

- Feeling powerless and trapped

- Shame about not having savings

After:

- Confidence that you can handle emergencies

- Options when problems arise

- Sense of control over your finances

- Pride in accomplishing a major goal

This isn’t just about the money—it’s about reclaiming your peace of mind.

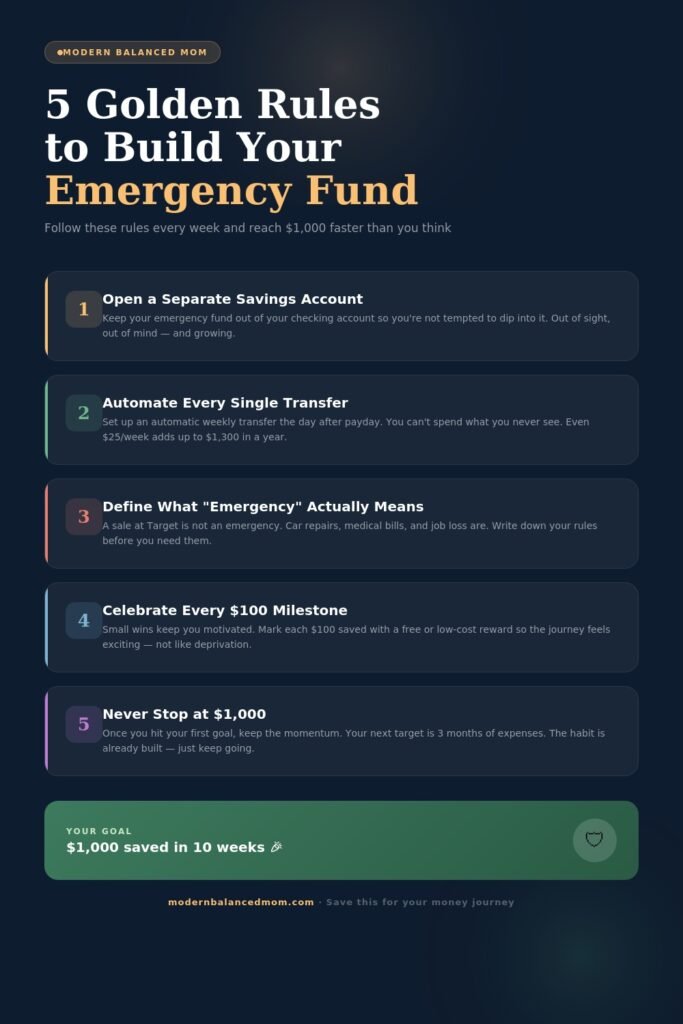

Before You Start: Set Up for Success

Jumping straight into saving without preparation sets you up to fail. Take Week 0 to lay the groundwork.

Week 0: Preparation Week

This week isn’t about saving money yet. It’s about creating the systems that make saving possible.

Action 1: Open a separate savings account

Why it matters: If your emergency fund sits in checking, you’ll spend it on non-emergencies.

How to do it:

- Online banks (Ally, Marcus, Discover) – No fees, higher interest

- Credit unions – Often no minimum balance

- Your current bank – Separate savings account, hidden from checking view

Goal: Money goes in, doesn’t come out unless it’s a true emergency

Action 2: Define what counts as an emergency

Write down your emergency criteria:

IS an emergency:

- Car breaks down and you can’t get to work

- Medical urgent care or ER visit

- Broken essential appliance (fridge, washer, heat/AC)

- Job loss

- Urgent home repair (burst pipe, no electricity)

NOT an emergency:

- Sale on something you want

- Holiday shopping

- Vacation

- Upgrading to a newer car

- “Just in case” purchases

Keep this list visible. When you’re tempted to dip into savings, check the list first.

Action 3: Track your current spending

For 5-7 days, write down every single dollar you spend.

Don’t change your behavior—just observe:

- Where is money going?

- What are you buying without thinking?

- What could be reduced or eliminated?

This awareness is crucial for finding money to save in the coming weeks.

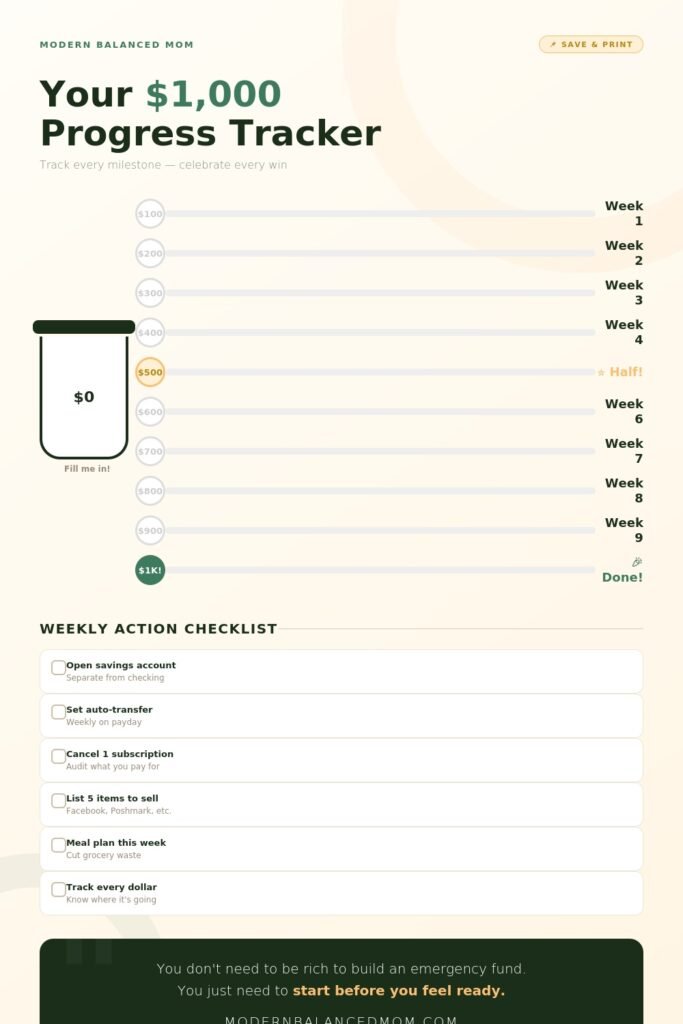

Action 4: Download and print your challenge tracker

Visual tracking is powerful.

Get a printable $1,000 challenge tracker (available at the end of this post) and put it somewhere visible—fridge, bathroom mirror, planner.

Every time you add money to savings, color in or check off the amount.

Seeing progress keeps you motivated when the journey feels long.

The 12-Week Action Plan

Here’s your week-by-week roadmap to $1,000. Each week includes specific actions and realistic savings goals.

Target: $83-85 per week (12 weeks to $1,000)

Some weeks you’ll save more, some less. The key is consistent progress.

Week 1: Find the Low-Hanging Fruit ($100 goal)

This week: Identify immediate cuts and quick wins

Action 1: Cancel unused subscriptions

Review your bank statements from the past month.

Look for:

- Streaming services you don’t watch

- Gym memberships you don’t use

- App subscriptions you forgot about

- Free trials that converted to paid

Average savings: $20-50/month

Action 2: Skip all eating out this week

Every coffee shop visit, lunch out, or dinner delivery = money to savings instead

Pack lunches. Make coffee at home. Cook simple dinners.

Average savings: $40-80 this week

Action 3: Sell something you don’t need

Look around your home:

- Clothes with tags still on

- Kids’ toys they’ve outgrown

- Electronics you don’t use

- Books, DVDs, games

Sell on:

- Facebook Marketplace (fastest)

- Poshmark (clothes)

- Decluttr (electronics, books)

- OfferUp (local pickup)

Average earnings: $30-100

Week 1 total saved: $90-230 (you’re already 9-23% there!)

Week 2: Trim Your Grocery Budget ($85 goal)

This week: Strategic grocery shopping

Action 1: Meal plan before shopping

Plan 5-6 simple dinners using:

- Ingredients you already have

- What’s on sale this week

- Budget-friendly proteins (chicken thighs, ground turkey, beans, eggs)

Action 2: Shop your pantry first

Before buying anything, use what you already own:

- That pasta in the back of the cupboard

- Frozen vegetables taking up freezer space

- Canned goods from six months ago

Action 3: Set a strict grocery budget

Challenge yourself: Cut your normal grocery spending by 25% this week

If you normally spend $150, aim for $110

Strategies:

- Buy store brand

- Skip convenience items (pre-cut veggies, pre-shredded cheese)

- No impulse purchases

- Stick to the list religiously

Average saved: $40-60 this week

Action 4: No-spend challenge

For the entire week, buy NOTHING except groceries and absolute necessities

No:

- Target runs “just to browse”

- Online shopping

- Coffee shops

- Convenience store stops

Average saved: $30-50

Week 2 total: $70-110 saved

Week 3: Bank a Windfall ($85 goal)

This week: Find money hiding in plain sight

Action 1: Collect and deposit all cash

Gather:

- Loose change throughout the house

- Cash in wallets, purses, coat pockets

- Coins in car cup holders

- Bills stuffed in drawers

Roll coins or use Coinstar (9% fee but instant), deposit everything

Average found: $20-50

Action 2: Return unused items

Look for:

- Items bought within return window (even without receipt, many stores give store credit)

- Gifts you won’t use

- Duplicate items

- Wrong sizes

Average returned: $25-75

Action 3: Pick up overtime or extra hours

If your job offers:

- Volunteer for overtime

- Pick up an extra shift

- Cover for a coworker

One extra shift or 4-5 overtime hours = $60-150 (after tax)

Action 4: Do a paid task or gig

Weekend side hustles:

- Babysit for a few hours

- Mow a neighbor’s lawn

- Clean someone’s house

- Run errands for elderly neighbors

Average earnings: $40-100

Week 3 total: $85-275 saved

Week 4: Cut Major Expenses ($85 goal)

This week: Negotiate and reduce bills

Action 1: Call your insurance company

Car and home insurance:

“I’m reviewing my budget and need to lower my insurance costs. What discounts am I eligible for? Can we adjust my coverage to reduce my premium?”

Common discounts:

- Bundling home and auto

- Paperless billing

- Pay-in-full discount

- Good driver discount

- Low mileage discount

Average savings: $20-60/month

Action 2: Review and reduce phone plan

Call your carrier or switch to a budget carrier:

Budget carriers (use major networks):

- Mint Mobile: $15-30/month

- Cricket: $30-55/month

- Visible: $25-45/month

If you’re paying $70+/month, you can cut this to $30-40

Average savings: $30-40/month

Action 3: Contact utility companies

Many utilities offer:

- Budget billing (evens out high/low months)

- Low-income assistance programs

- Payment plans that free up immediate cash

Call and ask: “What programs do you have to help reduce my monthly bill?”

Action 4: Pause or downgrade services

Temporarily pause:

- Hulu/Netflix/streaming (watch free options for a month)

- Gym membership (work out at home temporarily)

- Subscription boxes

Week 4 savings: $70-140 this month (bank first month’s savings to emergency fund)

Week 5-6: Lifestyle Adjustments ($170 total goal)

These two weeks: Sustained behavior changes

Week 5 Actions:

1. Pack all meals and snacks

- No buying lunch at work

- No vending machine

- No coffee shops

- Savings: $40-60

2. Free entertainment only

- Library instead of bookstore

- Parks instead of paid activities

- Free community events

- Home movie nights

- Savings: $30-50

3. DIY personal care

- Skip salon, do home haircuts or stretch appointments

- DIY nails

- At-home hair color

- Savings: $40-80

Week 5 total: $70-130

Week 6 Actions:

1. Transportation savings

- Carpool to work if possible

- Combine errands to reduce gas

- Skip unnecessary trips

- Savings: $20-40

2. Energy reduction

- Unplug devices not in use

- Lower/raise thermostat 2-3 degrees

- Shorter showers

- Run dishwasher/laundry only when full

- Savings: $15-30

3. Sell more items

- Continue decluttering and selling

- Kids’ clothes they’ve outgrown

- Kitchen items you don’t use

- Earnings: $30-60

Week 6 total: $65-130

Combined Week 5-6 savings: $135-260

Week 7-8: Income Boost ($170 total goal)

These two weeks: Bring in extra money

Week 7 Actions:

1. Freelance your skills

What can you do for money?

- Graphic design (Fiverr, Upwork)

- Writing/editing (Contently, ProBlogger)

- Virtual assistant work (Belay, Time Etc)

- Tutoring (Tutor.com, Wyzant)

- Pet sitting (Rover)

Even 3-5 hours = $50-150

2. Participate in paid studies

Research studies pay $50-200:

- User testing (UserTesting.com)

- Focus groups (FindFocusGroups.com)

- Medical studies (ClinicalTrials.gov)

- Market research (ResearchAndMe.com)

3. Gig economy work

Weekend or evening gigs:

- DoorDash/Uber Eats delivery

- Instacart shopping

- Task Rabbit tasks

- Rover dog walking

Week 7 earnings: $80-150

Week 8 Actions:

1. Cash in rewards

Check:

- Credit card rewards points (redeem for cash)

- Grocery store reward points

- Pharmacy rewards

- Old gift cards

Average: $20-50

2. Seasonal work

Many retailers hire temporary help:

- Weekend shifts at retail

- Event staffing

- Seasonal warehouse work

One weekend = $120-200

3. Yard sale or bulk selling

Gather everything sellable, host:

- Garage sale (in-person)

- Facebook Marketplace bulk lot

- Consignment shop drop-off

Average: $50-150

Week 8 earnings: $90-200

Combined Week 7-8 income: $170-350

Week 9-10: Deep Budget Cuts ($170 total goal)

These two weeks: Extreme frugality challenge

Week 9: Pantry Challenge

Goal: Spend $0 on groceries, eat only what you have

Rules:

- Use everything in pantry, fridge, freezer

- Get creative with combinations

- Only buy milk/bread if absolutely necessary

Savings: $80-150 (your normal grocery budget)

Week 10: No-spend week

Absolutely zero spending except:

- Bills already due

- Gas to get to work (only)

- Medications

Everything else = $0 spent

Strategies:

- Use up all leftovers

- Free entertainment only

- Avoid stores completely

- Unsubscribe from promotional emails

Savings: $50-100

Combined Week 9-10 savings: $130-250

Week 11-12: Final Push ($170 total goal)

These two weeks: Finish strong

Week 11 Actions:

Calculate your gap:

Where are you right now? How much more do you need to hit $1,000?

Deploy aggressive tactics:

1. Ask for help

- Take on extra work projects for bonuses

- Ask family for early birthday money (if applicable)

- Sell higher-value items (electronics, furniture you don’t need)

2. Maximize earnings

- Work every possible extra hour

- Do multiple gig jobs in one weekend

- Sell anything not nailed down

Week 11 goal: $85-100

Week 12 Actions:

Final sprint:

1. Analyze progress

If you’re close (within $50-100):

- One final push (extra shift, sell one more item)

- Cut spending to absolute zero

If you’re further away:

- Don’t panic—adjust your timeline

- Keep going, even if it takes 2-3 more weeks

- Progress is progress

2. Deposit that final amount

3. Celebrate your achievement

Week 12 goal: $70-100

Combined Week 11-12 savings: $155-200

Staying Motivated Through the Challenge

Twelve weeks is a long time to maintain intense focus. Here’s how to stay on track.

Track Progress Visually

Use your printable tracker daily:

Every deposit to savings:

- Color in the corresponding amount

- Calculate new total

- Write the date

Seeing the total climb keeps you going when motivation wanes.

Share Your Journey

Tell someone about your challenge:

Options:

- Accountability partner doing it with you

- Supportive friend who checks in weekly

- Online community (Facebook groups, Reddit)

- Social media updates (if you’re comfortable)

When others know, you’re less likely to quit.

Plan Mini-Celebrations

Hit milestones, celebrate (free/cheap ways):

$250: Family movie night at home

$500: Special home-cooked meal

$750: Day at a free local attraction

$1,000: Small celebration (within budget!)

Acknowledge progress without derailing it.

Remember Your “Why”

When tempted to quit or spend, revisit why this matters:

Your why might be:

- Never putting emergencies on credit cards again

- Sleeping at night without financial anxiety

- Having options when life happens

- Setting an example for your kids

- Breaking the paycheck-to-paycheck cycle

Write your “why” on your tracker. Read it when you’re struggling.

Adjust, Don’t Abandon

Some weeks you won’t hit the $85 target. That’s okay.

Life happens:

- Kids get sick

- Work is slower

- Unexpected expenses arise (ironic, right?)

If you have a low week:

- Don’t quit

- Adjust the timeline (add 1-2 weeks)

- Keep going

Saving $1,000 in 14 weeks instead of 12 is still a massive win.

What Counts as an Emergency (And What Doesn’t)

Now that you have $1,000 saved, you need clear rules about when to use it.

True Emergencies

Use your emergency fund for:

✓ Unexpected medical expenses (ER, urgent care, necessary prescriptions)

✓ Essential car repairs (you can’t get to work without it)

✓ Job loss (immediate needs while finding new work)

✓ Broken essential appliances (refrigerator, washer, heat/AC in extreme temps)

✓ Urgent home repairs (burst pipe, electrical failure, roof leak)

✓ Emergency pet care (life-threatening situation)

NOT Emergencies

Don’t use your emergency fund for:

✗ Holiday shopping

✗ Vacation

✗ Sale on something you want

✗ Upgrading functional items

✗ Non-essential cosmetic repairs

✗ Planned expenses you could have budgeted for

The Replacement Rule

If you do use emergency funds, immediately commit to replacing them.

Used $400 for car repair?

- Start a mini-challenge to rebuild that $400

- Same strategies, condensed timeline

- Goal: Back to $1,000 within 4-6 weeks

Your emergency fund should always replenish itself.

After You Hit $1,000: What’s Next?

Congratulations—you’ve saved $1,000! This is a massive achievement. But it’s not the finish line.

The Financial Journey Continues

Your next goals, in order:

1. Pay off high-interest debt (credit cards over 15% interest)

While keeping your $1,000 emergency fund intact, attack debt aggressively.

2. Build to 3-6 months of expenses

Once debt is gone, grow your emergency fund to cover 3-6 months of living expenses.

For a family spending $3,000/month:

- 3 months = $9,000

- 6 months = $18,000

This becomes your full emergency fund.

3. Save for specific goals

With debt gone and full emergency fund built:

- Down payment for house

- Kids’ college

- Retirement investing

- Vacation fund

The $1,000 emergency fund is your foundation. Everything else builds from here.

Don’t Stop the Habits

The behaviors that got you to $1,000 are the same behaviors that build wealth long-term:

✓ Intentional spending

✓ Saying no to unnecessary purchases

✓ Finding creative income sources

✓ Budgeting before spending

✓ Tracking progress

Keep these habits even after the challenge ends.

Common Challenges and Solutions

Let’s troubleshoot obstacles you’ll face.

Challenge #1: “I can’t find $85 per week”

Solution: Start smaller

Can’t find $85/week? Find what you CAN save:

- $50/week = $1,000 in 20 weeks (5 months)

- $30/week = $1,000 in 34 weeks (8 months)

- $20/week = $1,000 in 50 weeks (1 year)

Any progress toward $1,000 beats staying at $0.

Challenge #2: “An emergency happened during the challenge”

Solution: Handle it, then restart

If you have $400 saved and a $300 emergency hits:

- Use the $400 (that’s what it’s for)

- You now have $100

- Restart challenge from $100, not $0

You’re still ahead of where you started.

Challenge #3: “My partner isn’t on board”

Solution: Do it anyway

Ideal scenario: Partner joins you

Reality: You might be doing this alone

If your partner won’t participate:

- Save your portion of discretionary money

- Bank any windfalls that come to you

- Lead by example

When they see your $1,000, they might get inspired.

Challenge #4: “I’m a single parent with no margin”

This is the hardest situation and deserves acknowledgment.

Solutions:

- Extend timeline (18-24 weeks instead of 12)

- Focus on income side (side gigs, selling items)

- Utilize community resources (food banks, assistance programs) temporarily to free up cash

- Start with $500 as first goal, then build to $1,000

Even $25 saved per week = $1,000 in one year. It’s slower, but it’s still progress.

Your $1,000 Challenge Starts Now

You have everything you need:

✓ Week-by-week action plan

✓ Specific strategies for finding money

✓ Motivation techniques to stay on track

✓ Solutions to common obstacles

✓ Clear definition of true emergencies

The only thing left is to start.

Not next month when you “have more money.”

Not after the holidays.

Not when things are “less tight.”

Today. Right now.

Here’s what to do in the next 60 minutes:

- Open a separate savings account (online takes 10 minutes)

- Download and print your challenge tracker (link below)

- Find your first $20-50 (sell something, cancel a subscription, collect cash around the house)

- Deposit it immediately

- Mark it on your tracker

You’re officially $20-50 closer to your goal.

By this time next week, you could have $100 saved.

In 12 weeks, you could have $1,000.

In 6 months, you could have a full emergency fund.

It starts today.

Get Your Free $1,000 Challenge Tracker

Visual tracking makes this challenge achievable.

I’ve created a free printable $1,000 emergency fund challenge tracker to keep you motivated every single week.

What’s included:

✓ Weekly savings tracker with space to record each deposit

✓ Progress bar to color in as you save

✓ Milestone celebrations at $250, $500, $750, and $1,000

✓ Motivation prompts for difficult weeks

✓ Emergency definition checklist to keep you honest

✓ Weekly action items for all 12 weeks

Download it now, print it out, and put it somewhere visible.

Every time you add money to savings, mark it on the tracker. Watching that progress bar fill in creates momentum and accountability.

[DOWNLOAD FREE $1,000 CHALLENGE TRACKER]

This tracker has helped hundreds of moms save their first $1,000. Let it help you too.

The Life-Changing Power of $1,000

This isn’t just about money in a bank account.

Saving your first $1,000 emergency fund proves to yourself that:

✓ You CAN control your money

✓ You CAN delay gratification

✓ You CAN achieve hard financial goals

✓ You ARE capable of changing your family’s financial future

When the next emergency hits—and it will—you’ll have options instead of panic.

You’ll have security instead of stress.

You’ll have choices instead of being trapped.

That $1,000 emergency fund is your financial freedom fund.

It’s the foundation of every other financial goal you’ll ever achieve.

Start building it today.

Your future self is already thanking you.

Ready to save your first $1,000? Download the free challenge tracker, choose your Week 1 actions, and deposit your first $20-50 today. Share your starting point in the comments—we’re all cheering you on! You’ve got this.